Introduction

The key component of success and financial security is budgeting. Making a budget is the first step, regardless of your financial goals—whether they be to increase savings, lower debt, or just gain financial control. We’ll go over the fundamentals of budgeting, its significance, and how to make a budget that suits your needs in this guide.

What is Budgeting?

The process of organizing and controlling your earnings and outlays is known as budgeting. It enables you to keep tabs on your spending, make wiser financial choices, and reach your financial objectives. Living within your means and allocating money for investments and savings are guaranteed by a well-designed budget.

Why is Budgeting Important?

- Helps in Debt Avoidance: You can avoid overspending and lessen your dependency on credit cards or loans by keeping track of your spending.

- Promotes Savings: By allowing you to set aside a portion of your salary for savings, budgeting helps you maintain your financial stability.

- Decreases Stress: Financial tension is lessened and you feel more in control when you know where your money is going.

- Enhances Financial Planning: A budget aids in making plans for upcoming costs such as retirement, education, and vacations.

Steps to Create a Budget

- Evaluate Your Earnings

Knowing your income is the first step in creating a budget. Compute your entire monthly revenue, taking into account your salary, side gigs, freelancing, and any passive income.

- Monitor Your Spending

Make a list of every expense you incur, such as rent, utilities, groceries, insurance, entertainment, and subscriptions. Sort your expenditures into:

Rent, mortgage, insurance, and loan payments are examples of fixed expenses.

Travel, entertainment, eating out, and groceries are examples of variable costs.

You can find spending trends and places where you can make savings by keeping a few months’ worth of expense records.

- Establish Financial Objectives

Establish both immediate and long-term financial objectives. Saving for a trip or emergency fund are examples of short-term objectives, but retirement planning or home ownership are examples of long-term objectives. Setting up a budget aids in allocating funds for these objectives.

- Select a Method for Budgeting

Depending on your lifestyle, you can employ a variety of budgeting strategies:

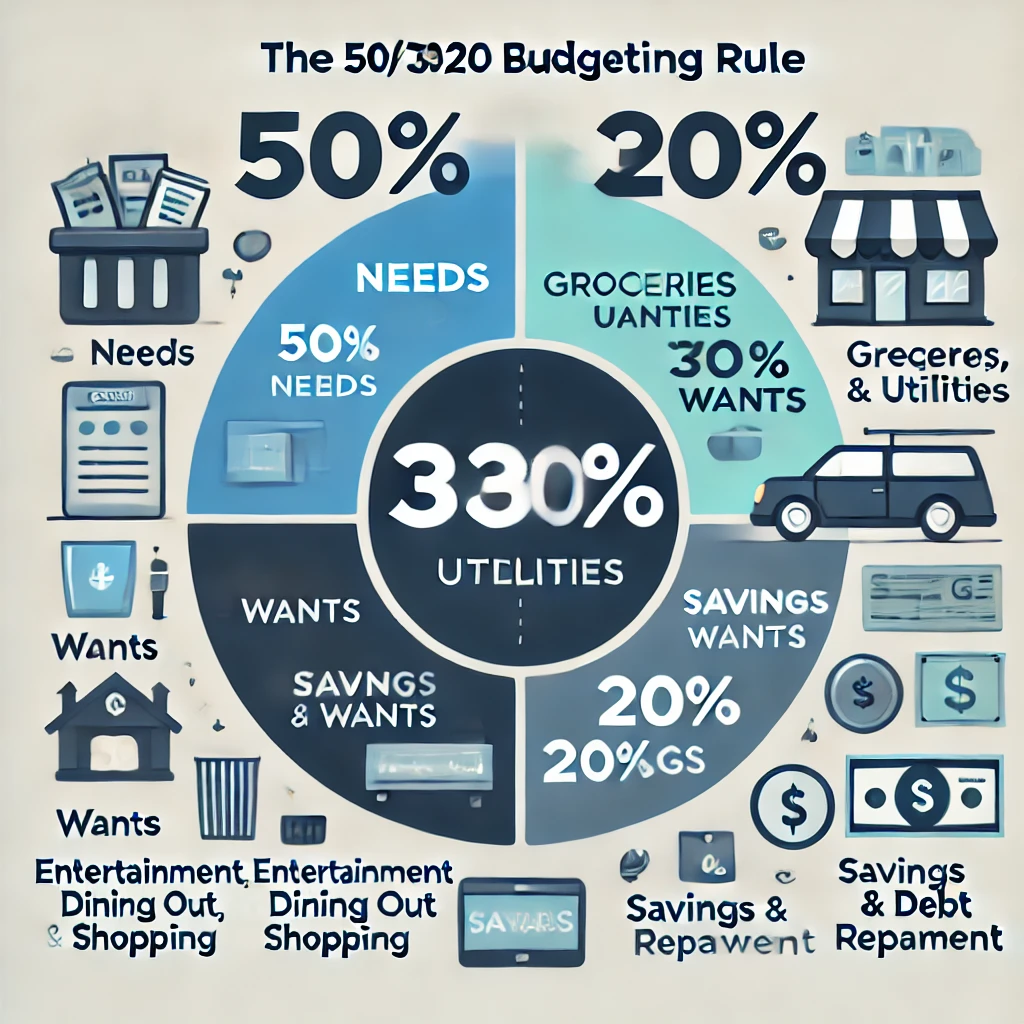

The 50/30/20 Rule

50% of revenue goes towards needs like groceries, rent, and bills.

30% goes into wants (buying, eating out, and entertainment).

20% for debt repayment and savings

A zero-based budget ensures that no funds are left unused by giving each dollar a specific purpose.

Envelope System: To reduce spending, cash is separated into envelopes for several expense categories.

- Reduce Needless Spending

Examine your expenditures and see where you might make savings. Think about cutting back on impulsive purchases, cooking at home rather than eating out, and terminating unwanted subscriptions.

- Establish an Emergency Fund

Your budget may be disrupted by unforeseen costs. To cover urgent repairs, job loss, or medical problems, try to accumulate at least three to six months’ worth of living expenses in an emergency fund.

- Regularly Review and Modify Your Budget

A budget needs to be updated on a regular basis; it is not a one-time plan. Review your expenditures at the end of each month and make any adjustments to your budget in light of any changes in your income, expenses, or financial objectives.

Apps & Tools for Budgeting

Budgeting is made simpler by technology. Think about utilizing apps such as:

Mint: Offers insights on budgeting and keeps track of spending.

You Need a Budget, or YNAB, assists you in allocating each dollar to a certain category.

PocketGuard: Shows how much is safe to spend, preventing overspending.

Budgeting templates that can be customized in Google Sheets or Excel.

Common Budgeting Mistakes to Avoid

Not Tracking Expenses: Overspending might result from not keeping an eye on your expenditures.

Creating Impractical Budgets: A budget need to be realistic and doable.

Ignoring Unexpected Costs: Budget for yearly or unforeseen costs, such as auto repair or hospital fees.

Ignoring Budget Adjustments: Your budget should adapt to life’s changes.

Conclusion

The ability to create a budget is crucial for gaining financial independence and taking charge of your money. You may lower debt, boost savings, and make plans for a secure future by making and following a budget. Begin now, maintain consistency, and see an improvement in your financial situation!

you can also read about What is Personal Finance